Many Americans have little to no emergency savings and face significant challenges dealing with even small financial shocks. Recent evidence from the Federal Reserve Board suggests that nearly half of adults in the U.S. could not cover an emergency expense requiring $400 without selling possessions or borrowing money. Though many have a desire to save, numerous would-be savers lack the required patience and self-control to follow through on such goals. Finding ways to overcome these difficulties and help individuals and families achieve their savings goals is of first order importance.

To help bridge this gap, researchers and practitioners have developed and tested numerous interventions that impose external discipline on savers by restricting access to deposited funds or placing heavy penalties on early withdrawals, with mixed success. Even when these interventions work, however, they tend to suffer from low take-up. Consumers who are highly impatient or cash-constrained may see little benefit in locking away savings. In addition, many financial institutions may be reticent to prevent clients from accessing their own funds.

In our recent paper “Soft Versus Hard Commitments: A Test on Savings Behaviors”, joint with Jill Luoto of RAND and Francisco Perez-Arce of CESR, we developed and tested a soft-commitment savings intervention designed to increase intrinsic motivation without imposing any external restrictions on behavior. In a six month online savings experiment, participants who expressed difficulty saving were randomly assigned to one of three conditions: a “traditional” savings account with no restrictions on withdrawals, a hard-commitment account where withdrawals were expressly prohibited, and a soft commitment account that was identical to the traditional savings account but included soft psychological pressure to save. Participants assigned to the soft commitment treatment were asked to think about their savings goals, how it would feel to achieve them, and make a pledge to work towards these goals.

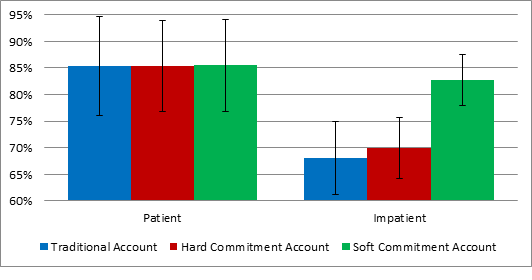

Individuals in the experiment were awarded money for participating in the study and given an opportunity to save a portion (or all) of their compensation in their randomly assigned savings account. We find that individuals assigned to the soft-commitment treatment saved significantly more of their allotted winnings initially than those assigned to either the hard-commitment or traditional account treatments. Strikingly, the effect was concentrated almost entirely on individuals who were prone to impatience. Patient individuals, measured using time preference elicitations, deposited the same amount of their compensation into their savings account regardless of treatment condition. Conversely, impatient individuals assigned to the soft-commitment treatment saved significantly more of their compensation than their counterparts in either the control or hard commitment treatments and saved a similar amount to individuals who are more patient.

Perhaps more importantly, the soft-commitment treatment led to statistically significant increases in amounts saved at the end of the study relative to participants who received no form of commitment. Like initial deposits, this effect was concentrated among individuals who were impatient and thus more likely to benefit from increased intrinsic motivation. Although the soft-commitment treatment induced higher initial deposits relative to the hard-commitment treatment, the high initial take-up combined with the illiquidity imposed by external restrictions resulted in the hard-commitment treatment yielding the highest overall savings by study’s end.

Though our experiment abstracted from a typical savings environment in a few important ways (participants were provided with funds to save and our savings accounts featured very high interest rates), our analysis suggests that simple techniques designed to increase intrinsic motivation can help improve savings behaviors, as can external restrictions that temporarily limit liquidity. Both findings are important as these techniques may help mitigate the chronic under-saving experienced by many Americans. Many institutions and organizations are unable (or unwilling) to develop and implement hard-commitment accounts that impose barriers to accessing resources, and many consumers are unwilling to participate in such accounts. The soft-commitment mechanisms we test, however, can be easily adopted by a variety of consumer facing organizations (for example, volunteer tax assistance sites and social service providers) and our findings suggest they are more palatable to a wider base of consumers. Moreover, these techniques can be implemented at very little cost, requiring at most a few minutes of interaction, and are easily scalable. Identifying low-cost, scalable interventions that can improve savings outcomes is of considerable importance for both policy and practice.

You must be logged in to post a comment.